How Much Will You Net Selling Your Home in Fort Lauderdale?

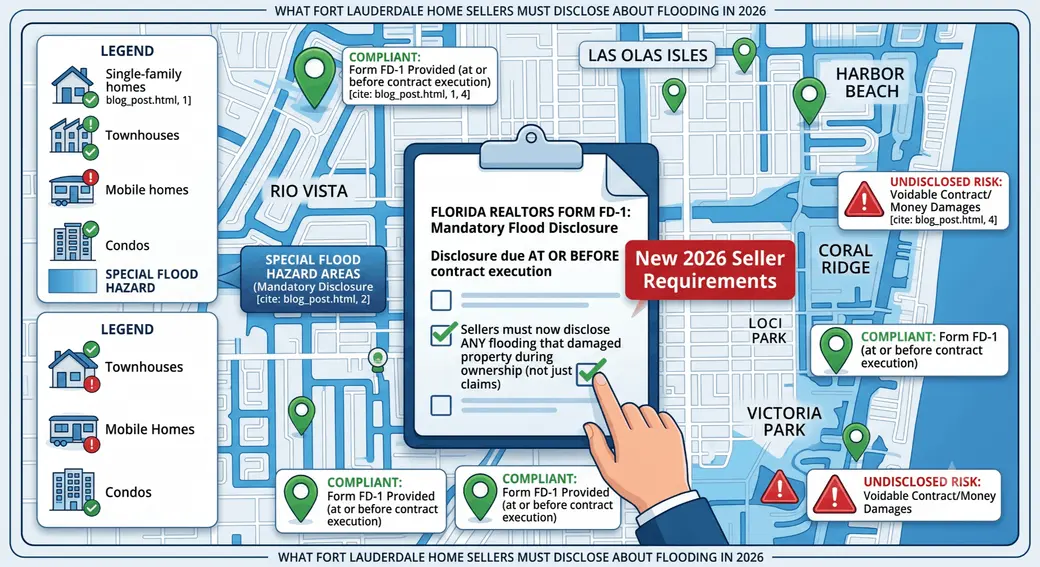

What Fort Lauderdale Home Sellers Must Disclose About Flooding in 2026

What Does Florida's Flood Disclosure Law Require From Sellers?

Florida requires all home sellers to complete a standalone Flood Disclosure form (Florida Realtors Form FD-1) and deliver it to the buyer at or before the sales contract is executed. As of October 1, 2025, the law expanded significantly: you must now disclose any flooding that damaged your property during your ownership — not just incidents that resulted in an insurance claim. Failure to disclose exposes you to a voidable contract and potential money damages.

If you're getting ready to list your Fort Lauderdale home — whether it's a single-family on a dry lot in Victoria Park, a canal-front property in Coral Ridge, or an Intracoastal estate in Harbor Beach — there's a disclosure requirement you cannot afford to get wrong.

Florida's flood disclosure law got a meaningful expansion in October 2025. The rules changed. What you're required to tell buyers is broader than it used to be. And in a city where a significant portion of homes sit inside or near FEMA Special Flood Hazard Areas, this isn't a technicality — it's one of the most consequential disclosures in your entire transaction.

Here's exactly what the law requires, what it means for Fort Lauderdale sellers, and how to protect yourself.

The FD-1 Form: What It Is and When It's Required

Florida Statute 689.302 requires sellers to provide a written flood disclosure to buyers. The standard form is Florida Realtors Form FD-1, updated in September 2025 to reflect the expanded requirements.

This form is standalone — it must be its own document, not buried inside the purchase contract. And it must be delivered at or before the moment the buyer signs the purchase agreement. Not at closing. Not during the inspection period. Before the contract is executed.

Every residential sale in Florida is covered — single-family homes, townhomes, condos, and mobile homes alike.

What the form requires you to disclose

Since October 1, 2025, sellers must answer yes or no to three core questions:

1. Have you ever filed an insurance claim for flood damage on this property?

This includes claims to NFIP (the National Flood Insurance Program), any private flood insurer, or homeowners insurance if flood damage resulted in a claim.

2. Have you ever received assistance to repair flood damage on this property?

Under the original 2024 law, this was limited to federal assistance. The 2025 expansion removed that restriction. Now you must disclose assistance received from any source — FEMA, state programs, a private grant, even a personal loan you took out specifically to repair flood damage.

3. Do you have knowledge of any flooding that damaged this property during your ownership?

This is the most significant change. You don't need to have filed a claim or received assistance — if flooding damaged your property and you know about it, you must disclose it. Period.

The form also requires you to acknowledge that standard homeowners insurance does not cover flood damage, and that buyers should consider purchasing separate flood insurance.

Why This Matters in Fort Lauderdale Specifically

Fort Lauderdale isn't just a coastal city — it's a city built on a network of canals. More than 165 miles of navigable waterways run through the city. Neighborhoods like Rio Vista, Las Olas Isles, Harbor Beach, Coral Ridge, and Lauderdale-by-the-Sea all include properties that sit in FEMA Special Flood Hazard Areas (SFHAs), primarily Zone AE or Zone VE.

Even properties away from the water can end up in moderate-risk zones. South Florida's flat topography and high water table mean flooding isn't limited to obvious waterfront locations — it can affect neighborhoods where you wouldn't expect it.

FEMA flood maps have also been in flux. Updated maps have changed zone designations for parts of Broward County in recent years, and properties that weren't previously in SFHAs are now classified differently.

Here's what that means as a seller: your buyer's lender almost certainly requires flood insurance if the property is in a SFHA with a federally backed mortgage. And the cost of that flood insurance — which can run $8,000–$20,000+ per year for a canal-front home, and higher for Intracoastal and oceanfront properties — is a major factor in whether a buyer can qualify or chooses to proceed.

If you don't disclose what you know about flooding, and the buyer finds out later — through an insurance claim, a neighbor, records, or after a storm — you're exposed to legal liability that doesn't disappear at closing.

The "As-Is" Misconception

This comes up constantly. Sellers assume that because they're selling the home under Florida's standard as-is contract, they're off the hook for disclosures. They're not.

An as-is sale means the buyer accepts the property in its current condition and the seller isn't obligated to make repairs. It does not mean the seller can conceal known material defects. Florida's disclosure duty — rooted in the Johnson v. Davis case from the 1980s — requires sellers to disclose facts that materially affect the value of the property, are not readily observable, and are not known to the buyer.

Flooding history absolutely qualifies. A buyer who discovers post-closing that you knew about water intrusion and didn't disclose it has legal recourse regardless of what the "as-is" language says.

The FD-1 form exists precisely because the standard as-is contract language wasn't enough to address Florida's specific flood risk reality.

What Happens If You Don't Disclose

If you fail to provide the FD-1 form — or if you complete it and omit known information — the consequences can be significant:

- The contract may be voidable. The buyer can walk away after signing if they discover the disclosure wasn't properly provided.

- Money damages. A buyer who discovers undisclosed flooding post-closing can sue for repair costs, diminished value, or related losses.

- Punitive damages are possible in cases where the court finds deliberate concealment.

- Professional consequences for the listing agent, potentially.

This isn't a risk worth taking. The FD-1 form exists to protect you as much as it protects the buyer — documenting exactly what you disclosed and when.

Practical Guidance for Fort Lauderdale Sellers

Start by thinking through your ownership history honestly. Did your backyard ever flood after a heavy storm? Did water intrude into the garage or any living space? Did you ever make repairs specifically related to water damage — new flooring after standing water, waterproofing work, landscaping regrading to redirect drainage? If any of that happened and it was flood-related, it likely needs to be on the form.

Check your records. Insurance policies, claim histories, permits, contractor invoices — pull what you have. Your disclosure should be based on what you actually know, not what you can prove, but documentation helps you answer questions accurately and supports your good faith in the event of a dispute.

Talk to your agent before listing. The FD-1 form needs to be completed before you accept an offer. Having it ready when the listing goes live — not scrambling to complete it mid-transaction — keeps the timeline clean and gives buyers full information upfront.

Know your flood zone. If you don't already know whether your property is in a SFHA, you can look it up through FEMA's Map Service Center at msc.fema.gov or through the City of Fort Lauderdale's GIS Flood Zones App. Knowing your zone helps you contextualize the disclosure and anticipate buyer and lender questions.

Fort Lauderdale participates in FEMA's Community Rating System at Class 7, which means properties in SFHAs can get approximately a 15% discount on NFIP flood insurance premiums. That's worth mentioning to buyers — it's a real benefit, and it can soften the conversation about flood insurance costs.

Consider pulling a current flood elevation certificate if you don't have one. For properties near the water or in flood zones, an elevation certificate documents where your lowest floor sits relative to base flood elevation. Properties above base flood elevation can qualify for significantly lower flood insurance premiums. If your home qualifies, this document can materially help your buyer's insurance picture.

Frequently Asked Questions

Yes. You still need to complete and provide the form. If your answers to all three questions are "no" — no claims, no assistance, no known flood damage — you complete the form accordingly and deliver it. The requirement is to provide the disclosure, not only to disclose problems. A clean FD-1 form actually helps your sale by giving the buyer documented confirmation.

The disclosure requires you to disclose flooding that damaged the property during your ownership. You aren't required to disclose history from before you took title. However, if you're aware of flooding history that predates your ownership — from a seller's disclosure you received when you bought — some agents recommend mentioning it anyway as a matter of good practice and transparency.

Florida's standard as-is contract includes an inspection period during which buyers can cancel for any reason. If flood-related issues surface during the inspection or if the buyer's insurance quotes come back higher than anticipated, they can walk during that period. The FD-1 form doesn't eliminate the buyer's right to cancel during inspection, but it does ensure the disclosure happened in writing, which protects you from post-closing claims.

It depends heavily on flood zone, elevation, construction type, and coverage amount. NFIP flood insurance in Broward County averages around $700–$2,500 per year for lower-risk zone properties, but can run $5,000–$20,000+ for canal-front and Intracoastal homes in higher-risk zones. Private flood insurance is worth comparing — rates vary significantly, and Fort Lauderdale's CRS Class 7 participation provides roughly a 15% NFIP discount in SFHAs.

Yes. The law requires disclosure of any flooding that damaged the property during your ownership — not just ongoing issues. The fact that you fixed it is relevant context, and your disclosure can note the repairs made. But omitting known historic flood damage because it's been repaired puts you at legal risk.

Selling a home in Fort Lauderdale means navigating Florida-specific disclosure requirements that are meaningfully more involved than what sellers in many other states deal with. The FD-1 flood disclosure is one piece of a broader picture that also includes the SPDR, radon disclosures, lead paint disclosures for pre-1978 homes, and pending code enforcement matters.

Getting ahead of these disclosures before you list — not scrambling through them once an offer comes in — keeps your transaction running smoothly and protects you from the kind of disputes that can derail a closing or show up months later.

If you're preparing to list your Fort Lauderdale or Broward County home and want to make sure your disclosure package is complete before you go to market, I'm happy to walk you through it. Reach out at scottsellsfl.com to schedule a pre-listing consultation.

Categories

- All Blogs (170)

- 01. Local News & Lifestyle (5)

- 02. Market Updates (21)

- 03. Home Prices & Inventory (10)

- 04. Mortgage & Interest Rates (11)

- 05. Affordability & Rent vs. Buy (8)

- 06. Buyer Tips, Myths & Guides (35)

- 07. Selling Tips, Myths & Guides (44)

- 08. Demographic Trends (11)

- 09. New Construction (7)

- 10. Real Estate News & Insights (14)

- 11. Featured Listings (1)

- 12. Community Spotlights (1)

- 13. Legal & Policy Updates (8)

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "