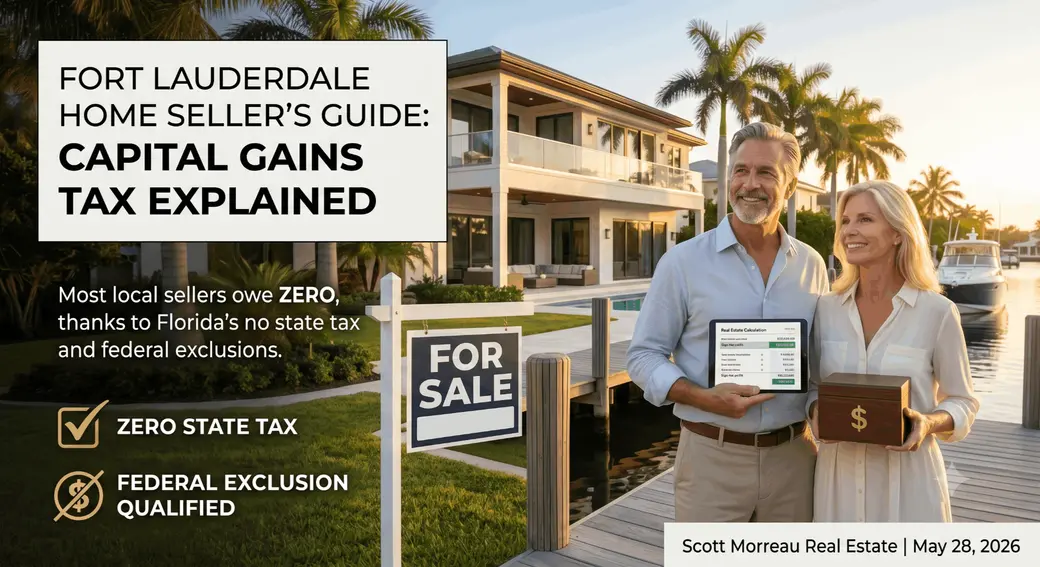

Capital Gains Tax When Selling Your Fort Lauderdale Home: What You Actually Owe

Capital Gains Tax When Selling Your Fort Lauderdale Home: What You Actually Owe

Do You Owe Capital Gains Tax When Selling Your Home in Fort Lauderdale?

Most Fort Lauderdale homeowners who have lived in their home for at least two of the last five years owe zero capital gains tax when they sell — federal or state. Florida has no state income tax, which means no state capital gains tax. On the federal side, the IRS Section 121 exclusion shields up to $250,000 of gain for single filers and $500,000 for married couples filing jointly. If your profit falls within those limits, you pocket it tax-free. If your gain exceeds those thresholds — which is increasingly common for long-term owners in Broward County's luxury market — you'll owe federal capital gains tax only on the portion above the exclusion.

By Scott Morreau | May 28, 2026

Here's what I hear all the time from sellers preparing to list in Fort Lauderdale:

"We've been here 15 years. The house has gone up a lot. Are we going to get hit with a huge tax bill?"

It's one of the most important questions to answer before you list — not after. And the answer is usually better than people expect, but not always simple.

Let's walk through exactly how this works, what the real numbers look like in Broward County's market, and where things get complicated.

The Good News: Florida Has No State Capital Gains Tax

Let's start with the part everyone misses. Florida doesn't tax capital gains. There's no state income tax here at all — which means when you sell your home, the state of Florida takes nothing from your profit. That's a meaningful advantage over sellers in states like California (which taxes capital gains at up to 13.3%), New York, or Massachusetts.

The only capital gains exposure for Fort Lauderdale home sellers is federal.

Who Qualifies for the Federal Exclusion

The IRS Section 121 exclusion lets you exclude a substantial portion of your home sale gain from federal taxes. The rules:

- $250,000 exclusion for single filers

- $500,000 exclusion for married couples filing jointly

- You must have owned the home for at least 2 years out of the last 5

- You must have lived in it as your primary residence for at least 2 of the last 5 years

- The ownership and residency periods don't have to be concurrent — they just both need to fall within that 5-year window

- You cannot have used this exclusion on another home sale within the past 2 years

For most Fort Lauderdale homeowners who've been in their primary residence for several years, this exclusion eliminates the federal tax bill entirely.

Here's a simple example at the lower end of Scott's market: You and your spouse bought a home in Victoria Park for $550,000 in 2016. You've lived there since. You sell today for $900,000. Your gain is $350,000. The $500,000 exclusion completely covers it. You owe nothing to the IRS.

Where It Gets Complicated: Long-Term Owners and Luxury Properties

The $500,000 cap matters a lot more in Broward County's current market than it did five or ten years ago.

Consider this scenario: A couple bought a waterfront home on Las Olas Isles in 2008 for $650,000. It's now worth $1.6 million. Their gain is $950,000. After the $500,000 exclusion, they have $450,000 of taxable gain. At the federal long-term capital gains rate — typically 15–20% depending on income — that's a federal tax bill between $67,500 and $90,000.

That's not a planning failure. That's a real outcome that surprises sellers who assumed the exclusion covered everything.

This is exactly the conversation I have with clients before we discuss list price. Your taxable gain affects your net, and your net affects your next move.

What Federal Long-Term Capital Gains Rates Look Like

If your gain exceeds the exclusion, the taxable portion is subject to federal long-term capital gains rates (assuming you've owned the home more than a year, which is almost always the case):

- 0% — for lower-income households (roughly under $94,000 in 2026 for married filers)

- 15% — for most middle and upper-middle income households (up to roughly $583,750 for married filers)

- 20% — for the highest earners

There's also the Net Investment Income Tax (NIIT) — an additional 3.8% federal tax that kicks in for high earners (above $250,000 single, $200,000 married filing separately, or $200,000 base with phase-outs) on investment income including real estate gains above the exclusion. So for some Fort Lauderdale luxury sellers, the effective marginal federal rate on excess gain could reach 23.8%.

None of this is state tax. It's all federal. Florida still takes nothing.

How to Calculate Your Capital Gain

Your capital gain is not simply the difference between your sale price and your original purchase price. The IRS definition of "gain" is:

Sale price − adjusted cost basis = capital gain

Your adjusted cost basis includes:

- Original purchase price

- Closing costs you paid when you bought

- Capital improvements you made (additions, a new roof, kitchen renovation, pool addition, impact windows)

- Points you paid on the original mortgage

What doesn't count: repairs and maintenance. Repainting, fixing a leak, replacing a water heater — these are expenses, not basis additions. But replacing the entire HVAC system, adding a bathroom, or installing impact-rated windows? Those increase your basis and reduce your taxable gain.

If you've been in your Fort Lauderdale home for 10–20 years, there's a good chance you've added significant improvements that you haven't tracked carefully. That's worth piecing back together with your CPA before you close — it can move your taxable gain by $30,000, $50,000, or more.

Investment Properties and Second Homes: Different Rules Apply

Everything above applies to your primary residence. If you're selling a rental property, investment property, or vacation home you don't use as a primary residence, the exclusion doesn't apply. Your entire gain is taxable — and you also face depreciation recapture, which taxes the depreciation deductions you took (or should have taken) over the years at up to 25%.

For investment property sellers, the most powerful planning tool is often the 1031 exchange — which allows you to defer capital gains by rolling proceeds into a like-kind replacement property within specific time windows (45 days to identify a replacement property, 180 days to close). This is a complex strategy that requires a qualified intermediary and a tax advisor, but it's one I help clients think through as part of the pre-listing conversation.

I've worked with a number of Broward County investors who've used 1031 exchanges to defer significant six-figure gains while repositioning into stronger properties. The timing is strict, so the planning has to start before the listing goes live. You can read more about how net proceeds work on a standard home sale in my earlier post on how much you'll net selling your Fort Lauderdale home.

Timing Matters: The 2-Year Residency Rule and Partial Exclusions

You don't have to have lived there exactly two consecutive years. The 2-year use test is measured by aggregate time within the 5-year window. Even if you moved out for a period, you might still qualify if you total at least 24 months of residency across the lookback window.

If you fall short of the full 2-year residency test — maybe you need to move for a job, a health situation, or an unforeseen life change — you may still qualify for a partial exclusion. The IRS allows a prorated exclusion based on how many months you lived there relative to 24. It's not nothing.

This is a fact-specific calculation, and your CPA needs to run the actual numbers. But the point is: don't assume you get zero just because you haven't hit the full two years.

The Practical Planning Conversation

Here's what I tell every client who raises this question:

The conversation with your CPA needs to happen before your listing goes live, not after you've accepted an offer. Once you're under contract, you're reacting. If you plan ahead, you might have options — adjusting timing to hit the 2-year mark, tracking down basis improvements to reduce taxable gain, or structuring the transaction in a way that works better for your situation.

For most Fort Lauderdale sellers in the $750K–$1.5M range who've owned for several years, the exclusion covers the full gain and there's no federal tax at all. For longer-term owners of higher-value homes — especially in waterfront neighborhoods like Harbor Beach, Rio Vista, and Las Olas Isles — the gain may exceed the exclusion, and the planning matters.

Either way, knowing your number before you list puts you in a much better position to make decisions about pricing, timing, and what to do next.

Frequently Asked Questions

Does Florida have a capital gains tax on home sales?

No. Florida has no state income tax and no state capital gains tax. When you sell your Fort Lauderdale or Broward County home, the state of Florida takes nothing from your profit — regardless of how much you made on the sale. Your only potential tax liability is federal.

What is the Section 121 exclusion and how much can I exclude?

The IRS Section 121 exclusion lets single filers exclude up to $250,000 of home sale gain from federal capital gains tax, and married couples filing jointly can exclude up to $500,000. To qualify, you must have owned the home and used it as your primary residence for at least 2 of the last 5 years before the sale. If your gain falls within those limits, you owe no federal capital gains tax.

What if my gain is more than $500,000?

Only the amount above the exclusion is taxable. For example, if a married couple has a $700,000 gain, the first $500,000 is excluded, and only the remaining $200,000 is subject to federal capital gains tax — typically at 15–20% depending on your income level. Some high earners also pay an additional 3.8% Net Investment Income Tax on the taxable portion.

What improvements can I add to my cost basis to reduce my taxable gain?

Capital improvements — additions, room conversions, new roofs, pool installations, impact windows, major system replacements (HVAC, electrical, plumbing) — all increase your adjusted cost basis and reduce your taxable gain. Repairs and routine maintenance do not qualify. Keep records and receipts, and work with your CPA to document improvements before closing.

What are the capital gains rules if I'm selling a rental property in Fort Lauderdale?

Investment properties and rental homes do not qualify for the Section 121 primary residence exclusion. Your entire gain is taxable, and you may also owe depreciation recapture tax (up to 25%) on the depreciation deductions you've taken over the years. A 1031 exchange is often the most effective strategy for deferring this tax — but it requires planning before you sell, not after. Consult a qualified tax advisor and intermediary before listing.

Know Your Number Before You List

Capital gains tax is one of those topics where the answer is often better than sellers fear — but the times when it does apply, the stakes are high. Running the numbers before you list means you can price strategically, time your sale if it matters, and walk into closing without any surprises.

If you're thinking about selling in Fort Lauderdale, Wilton Manors, or anywhere in Broward County and want to understand what you'll net — after commissions, closing costs, and any applicable taxes — I'm happy to walk you through a complete pre-listing analysis. Reach out at scottsellsfl.com to schedule a call.

Note: This post is for general informational purposes and does not constitute tax or legal advice. Please consult a qualified CPA or tax attorney regarding your specific situation.

Categories

- All Blogs (170)

- 01. Local News & Lifestyle (5)

- 02. Market Updates (21)

- 03. Home Prices & Inventory (10)

- 04. Mortgage & Interest Rates (11)

- 05. Affordability & Rent vs. Buy (8)

- 06. Buyer Tips, Myths & Guides (35)

- 07. Selling Tips, Myths & Guides (44)

- 08. Demographic Trends (11)

- 09. New Construction (7)

- 10. Real Estate News & Insights (14)

- 11. Featured Listings (1)

- 12. Community Spotlights (1)

- 13. Legal & Policy Updates (8)

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "