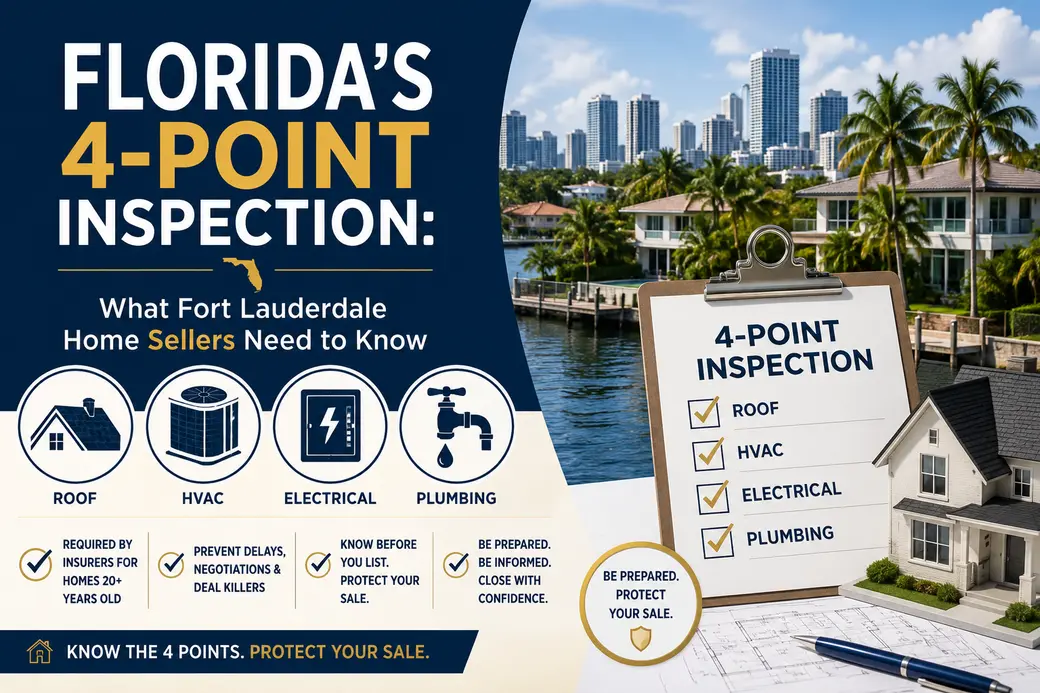

Florida's 4-Point Inspection: What Fort Lauderdale Home Sellers Need to Know

Florida's 4-Point Inspection: What Fort Lauderdale Home Sellers Need to Know

What Is a 4-Point Inspection in Florida, and Why Do Sellers Need to Know About It?

A 4-point inspection is a focused review of four home systems — roof, HVAC, electrical, and plumbing — that Florida insurance companies require before writing a new homeowners policy on most homes 20 years or older. As a seller, this matters because your buyer's insurer will order one, and if something fails, the buyer may be unable to get coverage, their lender will block the loan, and your deal can fall through. In Fort Lauderdale and Broward County, where much of the housing stock was built in the 1960s through 1990s, the 4-point inspection is one of the most common friction points in a transaction.

By Scott Morreau | May 6, 2026

If you're selling a home in Fort Lauderdale, Victoria Park, Coral Ridge, Wilton Manors, or anywhere else in Broward County — and your home is more than 20 years old — there's a very good chance a 4-point inspection is going to become part of your transaction.

Most sellers don't know this until they're already under contract. That's when the surprises start.

Here's what you need to understand before you list.

What the 4-Point Inspection Actually Covers

The name says it all: the inspection covers four systems.

Roof. The inspector notes the roof material, age, and condition, and estimates remaining useful life. This is the most scrutinized component in Florida. Insurers are aggressive about roof age — many won't write new policies on roofs over 15 to 20 years old, regardless of condition. A roof over 20 years is often flagged automatically.

HVAC. The inspector photographs the air handler and condenser unit and reads the manufacture date from the data plate. Most insurers want to see a system with at least 5 years of remaining life. A unit from 2005 raises questions; one from 1998 is a problem.

Electrical. This is where deals get complicated. Inspectors look for the type of panel, the wiring material, and any obvious hazards. Federal Pacific and Zinsco panels — which were common in Florida homes built between the 1950s and 1980s — are frequently declined by insurers. Aluminum branch circuit wiring is another red flag. Both can result in an outright coverage denial.

Plumbing. Inspectors evaluate pipe material and check for signs of leaks. Polybutylene pipes — widely installed in Florida homes from the mid-1970s through the early 1990s — are the primary concern here. Many insurers won't cover homes with polybutylene pipes at all.

A 4-point typically costs $75 to $150 in Broward County and takes about 45 minutes. It's not the same as a full home inspection — it's specifically for insurance underwriting.

Why This Is a Seller Problem, Not Just a Buyer Problem

Here's the sequence that trips sellers up.

Your buyer makes an offer. You accept. They go under contract with a financing contingency. Their lender requires homeowners insurance as a condition of funding. Their insurance agent orders a 4-point inspection. The inspector flags a 22-year-old roof, aluminum wiring in the panel, and a 2001 AC unit.

The insurer declines coverage.

Without coverage, the lender won't fund. Without funding, there's no closing.

At that point, you're looking at one of three outcomes: negotiate a price reduction or repair credit, make the repairs yourself before closing, or lose the buyer entirely. If the buyer walks, you restart the marketing process — with a listing that's been under contract and fallen through.

This scenario plays out in Broward County more than most sellers expect. Homes in Fort Lauderdale neighborhoods like Victoria Park, Coral Ridge, Rio Vista, and Harbor Beach were largely built between the 1950s and 1980s. Beautiful homes — but many with original or aging electrical panels, old plumbing, and roofs approaching the end of their useful life.

To put the roof issue in concrete terms: if your roof is 20 years old and a replacement runs $18,000 to $30,000 in today's market, that's a real number that will show up in your net proceeds calculation. How much will you actually net from your Fort Lauderdale sale? — that post walks through the full math.

What to Do Before You List

The best time to deal with a 4-point is before you accept an offer — not after.

Order your own 4-point inspection pre-listing. For $75 to $150, you get the same report the buyer's insurer will see. If there are issues, you have time to address them on your schedule rather than under contract pressure.

Pair it with a wind mitigation inspection. These are often done at the same time and typically run $100 to $150 as a bundled service. A wind mitigation report documents your roof's construction, deck attachment, roof-to-wall connections, and opening protection (impact windows, shutters). A strong wind mitigation report can save your buyer 10% to 40% or more on their annual insurance premium — which is a real selling point in a market where Broward County insurance costs still run $4,000 to $7,000+ per year on many homes.

Know your roof's age before your buyer does. If you don't know when your roof was last replaced, check your permit history through the Broward County Building Division. If your roof is 15 to 18 years old, budget the conversation — your buyer's insurer will flag it, and you want to respond with an inspection showing remaining useful life rather than being caught off-guard.

Address flagged issues strategically. Not every 4-point issue is worth fixing. A 15-year-old AC unit in good working condition may get through with documentation of recent maintenance. A Federal Pacific panel, on the other hand, is routinely declined by insurers — and replacing it typically runs $3,500 to $5,500, which is often worth doing before listing rather than handing that negotiation to a buyer under contract.

The Broward Insurance Picture in 2026

One piece of good news for sellers this year: homeowners insurance costs in Broward County are coming down. Citizens Property Insurance — Florida's insurer of last resort, which covers a large share of Broward homes — announced rate reductions averaging 14.1% for Broward policyholders beginning June 1, 2026. That's the largest county-level reduction in the state, driven by litigation reforms that have brought 17 new carriers into the Florida market.

For sellers, this matters. Fewer buyers getting scared off by insurance costs means slightly easier qualification conversations and a bit more demand in your price range. But roof age and panel issues haven't gone away — insurers are still underwriting carefully, and a bad 4-point will still derail a deal.

The insurance news is a tailwind. A failing 4-point is still a headwind. The sellers who are winning right now are the ones who've done the prep work.

Frequently Asked Questions

What triggers a 4-point inspection in a Florida home sale?

The buyer's insurance company triggers it, typically for any home that's 20 years old or older. Citizens Property Insurance requires a 4-point for homes 20 years and older on all new applications. Most private carriers have similar requirements. In a typical Fort Lauderdale transaction on a home built before 2005, plan on a 4-point being ordered.

What happens if the 4-point inspection fails?

If the insurer declines coverage based on the 4-point findings, the buyer's lender will not fund the loan. This usually triggers a renegotiation — the buyer may request a repair credit or price reduction, or may be entitled to cancel the contract and recover their deposit. The deal is not automatically dead, but it creates significant pressure on the seller to either make repairs or adjust the price.

Should I get a 4-point inspection before listing my Fort Lauderdale home?

Yes, particularly if your home is more than 20 years old or if you know any of the four systems are aging. A pre-listing 4-point runs $75 to $150 and gives you time to address problems before they become contract-stage emergencies. It's one of the highest-ROI things a Fort Lauderdale seller can do before going to market.

What are the most common reasons a 4-point inspection fails in Florida?

The most frequent failure points are: roofs over 15 to 20 years old, Federal Pacific or Zinsco electrical panels, aluminum branch circuit wiring, polybutylene pipes, and HVAC systems 15+ years old. Roofs and electrical panels are the two issues most likely to result in outright insurance denial.

Does a wind mitigation inspection help with the 4-point?

They're separate inspections that serve different purposes. The 4-point determines insurance eligibility; the wind mitigation determines your insurance rate discount. Getting both done at the same time — typically $200 to $250 combined — is smart pre-listing practice. A strong wind mitigation report can reduce your buyer's insurance premium by 10% to 40% and makes your home noticeably more attractive to financed buyers in Broward County.

The bottom line: if you're preparing to list a home in Fort Lauderdale, Wilton Manors, Oakland Park, or anywhere in Broward County — and your home is more than 20 years old — a 4-point inspection isn't optional. It's part of every transaction. The only question is whether you deal with it proactively or reactively.

Sellers who go into the process informed, with the inspection already done and issues already addressed, close faster, negotiate from a stronger position, and net more.

If you'd like to talk through what your pre-listing preparation should look like — including whether your systems are likely to pass, what repairs are worth making, and how to price your home with full knowledge of your costs — I'm happy to walk you through it. Reach out at scottsellsfl.com.

About Scott Morreau

Scott Morreau, PA is a top-rated Realtor® and Broker Associate with Real Broker, LLC, specializing in residential real estate across Fort Lauderdale, Wilton Manors, Oakland Park, Pompano Beach, Dania Beach, and Broward County. Licensed since 2001 and active in South Florida since 2006, Scott has closed over $52 million in Florida real estate — including $7.1 million in the past year — and is ranked among the top 500 agents in the region with 70+ five-star reviews. Scott specializes in luxury and waterfront homes, investment properties and 1031 exchanges, relocation to and from South Florida, and serving LGBTQ+ clients, and is known for his concierge-level preparation and client-first philosophy he calls A Better Real Estate Experience.

Categories

- All Blogs (167)

- 01. Local News & Lifestyle (5)

- 02. Market Updates (21)

- 03. Home Prices & Inventory (10)

- 04. Mortgage & Interest Rates (11)

- 05. Affordability & Rent vs. Buy (8)

- 06. Buyer Tips, Myths & Guides (34)

- 07. Selling Tips, Myths & Guides (42)

- 08. Demographic Trends (11)

- 09. New Construction (7)

- 10. Real Estate News & Insights (13)

- 11. Featured Listings (1)

- 12. Community Spotlights (1)

- 13. Legal & Policy Updates (7)

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "